An Income Statement is one of the most common reports in accounting. As a business owner, you have no doubt looked at your income statement. But we like to get back to basics here at Beyond, so we are discussing: What is an income statement? What should you look at when reviewing your income statement? And how can you listen to the story your income statement is telling you?

What is an Income Statement?

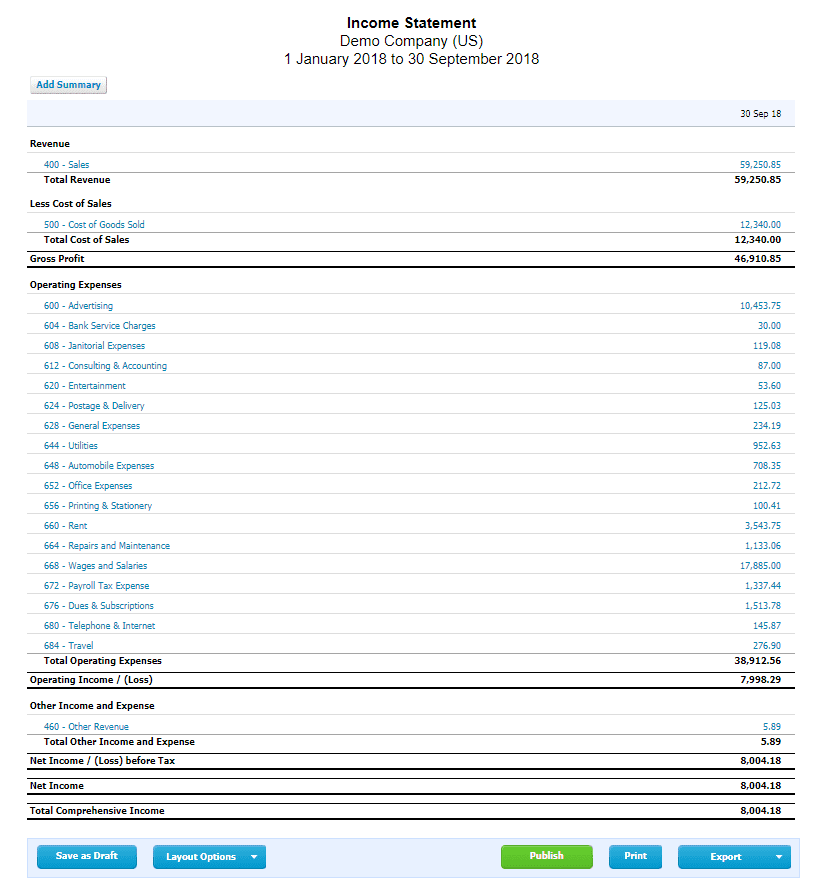

The income statement is sometimes also referred to as the profit and loss statement or as the P&L. The income statement reports on you how your business performed for a specific period of time. The income statement reports the revenue, cost of goods sold, gross profit, expenses, net income and other totals for the period of time shown in the heading of the report.

Let’s define the income statement section by section:

- Revenue: Fees earned from the sale of a product or from providing services

- Cost of Goods Sold: Direct cost related to the sale of the product or service

- Gross Profit: The net total of Revenue – Cost of Goods Sold

- Expenses: Indirect costs related to the primary operations of the business

- Operating Income/Loss: The net total of Gross Profit – Expenses

- Other Income: Revenue that is not related to the primary operations of the business

- Other Expense: Expenses that are not directly related to the primary operations of the business

- Net Income/Loss: The net total of Operating Income/Loss + Other Income – Other Expense

What should you look at when reviewing your income statement?

In our experience, most business owners first look at the total revenue and then go straight to the “bottom line” to see the net income or net loss. However, part of getting back to basics with your financial reporting is getting the complete picture, not just a part of it.

Total revenue is only telling you part of the story. Your revenue could appear to be quite high, but if your cost of goods is high in relation to your revenue and/or if your expenses are exceeding your revenue, you could be in trouble.

The net income or net loss is a very important total to look at. Most business owners would hope to see a positive amount or net income on their income statement. But again the net income is only telling you part of the story.

Let’s say you are the sole proprietor, who is not on the payroll, of a small business which shows a positive net income for the period. The amount of the net income needs to be enough to properly compensate you for your time and investment in the business.

What if your income statement shows that you had a net loss for the period? Again this might only be telling you part of the story. Perhaps your business has slow periods during certain times of the year. A net loss on the income statement could be related to the period of time being reported.

How can you listen to the story your income statement is telling?

The income statement provides you with a way to measure things. The story your income statement is telling you can be invaluable. Is your revenue high enough to cover your expenses? Are you making a profit with the business? Where are you spending your money? Are there expenses that you could reduce?

One thing that we like to do is to compare revenue and expenses from a prior period to the current period. This can help to see if revenue has grown or expenses have jumped. Many business owners focus solely on increasing revenue but reviewing your expenses and determining areas that you could cut back can be just as important.

Sometimes it might feel like your accounting reports are written in a different language. But we can be on your team to help you understand the story that your accounting reports are trying to tell you. Would you like to “get back to basics” and explore how we can help you? If so, please contact us today for a free consultation.